Recursive partitioning:also known as divide and conquer because it splits the data into subsets, which are then split repeatedly into even smaller subsets, and so on and so forth until the process stops when the algorithm determines the data within the subsets are sufficiently homogenous, or another stopping criterion has been met.

Divide and conquer might stop at a node in a case that:

- All (or nearly all) of the examples at the node have the same class

- There are no remaining features to distinguish among the examples

- The tree has grown to a predefined size limit

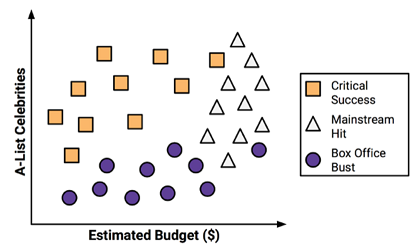

A case example of divide and conquer

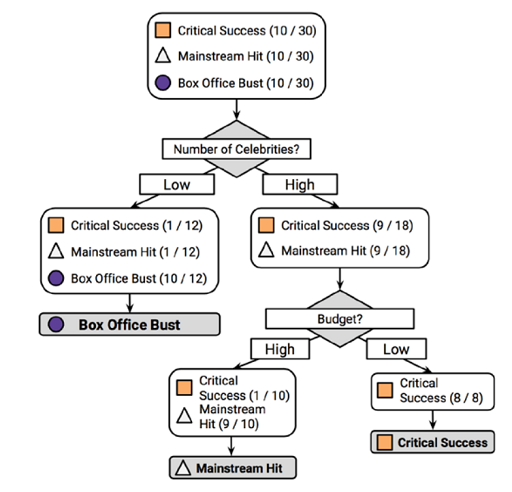

Decide to develop a decision tree algorithm to predict whether a potential movie would fall into one of three categories: Critical Success, Mainstream Hit, or Box Office Bust.

- produce a scatterplot to illustrate the pattern:

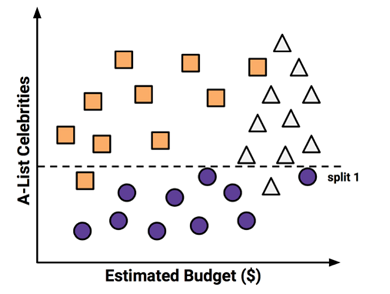

2a. Using the divide and conquer strategy, we can build a simple decision tree. To create the tree’s root node, we split the feature indicating the number of celebrities, partitioning the movies into groups with and without a significant number of A-list stars:

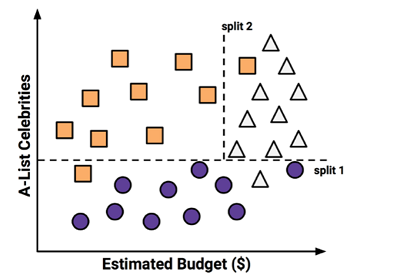

2b. Next, among the group of movies with a larger number of celebrities, we can make another split between movies with and without a high budget:

We have partitioned the data into three groups.

- The group at the top-left corner of the diagram is composed entirely of critically acclaimed films. This group is distinguished by a high number of celebrities and a relatively low budget.

- At the top-right corner, majority of movies are box office hits with high budgets and a large number of celebrities.

- The final group, which has little star power but budgets ranging from small to large, contains the flops.

It is not advisable to overfit a decision tree in this way since more than 80 percent of the examples in each group are from a single class. This forms the basis of our stopping criterion.

The C5.0 decision tree algorithm

A simple tree

The C5.0 decision tree algorithm

Choosing the best split

- Identify which feature to split upon. The degree to which a subset

of examples contains only a single class is known as

purity, and any subset composed of only a single class is calledpure. - Entropy quantifies the randomness, or disorder, within a set of class values. Sets with high entropy are very diverse and provide little information about other items that may also belong in the set, as there is no apparent commonality. The decision tree hopes to find splits that reduce entropy, ultimately increasing homogeneity within the groups.

-

Entropy is measured in bits. If there are only two possible classes, entropy values can range from 0 to 1. For n classes, entropy ranges from 0 to log2(n). In each case, the minimum value indicates that the sample is completely homogenous, while the maximum value indicates that the data are as diverse as possible.

For a given segment of data (S), the term c refers to the number of

class levels and Pi refers to the proportion of values falling into

class level i. For example, suppose we have a partition of data with

two classes: red (60 percent) and white (40 percent). We can calculate

the entropy as follows:

-0.60 * log2(0.60) - 0.40 * log2(0.40)

## [1] 0.9709506

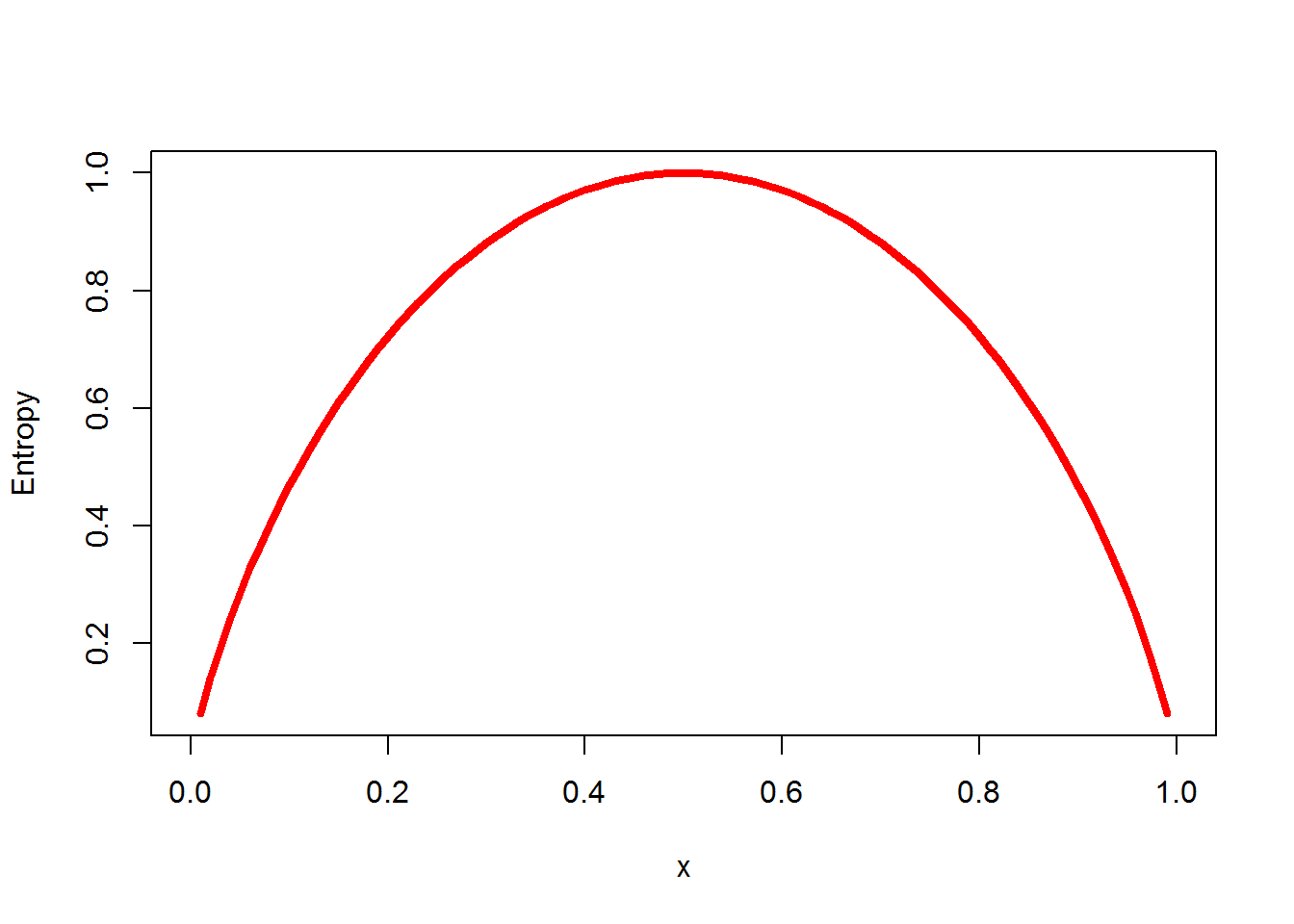

# Examine the entropy for all the possible two-class arrangements

curve(-x * log2(x) - (1 - x) * log2(1 - x), col = "red", xlab = "x", ylab = "Entropy", lwd = 4)

- A 50-50 split results in maximum entropy. As one class increasingly dominates the other, the entropy reduces to zero

Information gain to use entropy to determine the optimal feature to

split upon. The information gain for a feature F is calculated as the

difference between the entropy in the segment before the split (S1) and

the partitions resulting from the split (S2):

InfoGain*(*F*)=*Entropy*(*S*1)−*Entrop**y(S2)

One complication is that after a split, the data is divided into more than one partition. Therefore, the function to calculate Entropy(S2) needs to consider the total entropy across all of the partitions. It does this by weighing each partition’s entropy by the proportion of records falling into the partition.

- The total entropy resulting from a split is the sum of the entropy of each of the n partitions weighted by the proportion of examples falling in the partition (wi).

- The higher the information gain, the better a feature is at creating homogeneous groups after a split on this feature. If the information gain is zero, there is no reduction in entropy for splitting on this feature.

Pruning the decision tree

The process of pruning a decision tree involves reducing its size such that it generalizes better to unseen data.

Two Solutions:

Early stopping or pre-pruning the decision tree:

stop the tree from growing once it reaches a certain number of decisions or

when the decision nodes contain only a small number of examples.

(But there is no way to know whether the tree will miss subtle, but

important patterns that it would have learned had it grown to a

larger size.) #### **Post-pruning**

involves growing a tree that is intentionally too

large and pruning leaf nodes to reduce the size of the tree to a

more appropriate level

Example - identifying risky bank loans using C5.0 decision trees

Step 1 - collecting data

The credit dataset includes 1,000 examples on loans, plus a set of numeric and nominal features indicating the characteristics of the loan and the loan applicant. A class variable indicates whether the loan went into default

Step 2 - exploring and preparing the data

Ignore the stringsAsFactors option as the majority of the features in the data are nominal:

credit <- read.csv("credit.csv")

str(credit)

## 'data.frame': 1000 obs. of 17 variables:

## $ checking_balance : Factor w/ 4 levels "< 0 DM","> 200 DM",..: 1 3 4 1 1 4 4 3 4 3 ...

## $ months_loan_duration: int 6 48 12 42 24 36 24 36 12 30 ...

## $ credit_history : Factor w/ 5 levels "critical","good",..: 1 2 1 2 4 2 2 2 2 1 ...

## $ purpose : Factor w/ 6 levels "business","car",..: 5 5 4 5 2 4 5 2 5 2 ...

## $ amount : int 1169 5951 2096 7882 4870 9055 2835 6948 3059 5234 ...

## $ savings_balance : Factor w/ 5 levels "< 100 DM","> 1000 DM",..: 5 1 1 1 1 5 4 1 2 1 ...

## $ employment_duration : Factor w/ 5 levels "< 1 year","> 7 years",..: 2 3 4 4 3 3 2 3 4 5 ...

## $ percent_of_income : int 4 2 2 2 3 2 3 2 2 4 ...

## $ years_at_residence : int 4 2 3 4 4 4 4 2 4 2 ...

## $ age : int 67 22 49 45 53 35 53 35 61 28 ...

## $ other_credit : Factor w/ 3 levels "bank","none",..: 2 2 2 2 2 2 2 2 2 2 ...

## $ housing : Factor w/ 3 levels "other","own",..: 2 2 2 1 1 1 2 3 2 2 ...

## $ existing_loans_count: int 2 1 1 1 2 1 1 1 1 2 ...

## $ job : Factor w/ 4 levels "management","skilled",..: 2 2 4 2 2 4 2 1 4 1 ...

## $ dependents : int 1 1 2 2 2 2 1 1 1 1 ...

## $ phone : Factor w/ 2 levels "no","yes": 2 1 1 1 1 2 1 2 1 1 ...

## $ default : Factor w/ 2 levels "no","yes": 1 2 1 1 2 1 1 1 1 2 ...

table(credit$checking_balance)

##

## < 0 DM > 200 DM 1 - 200 DM unknown

## 274 63 269 394

table(credit$savings_balance)

##

## < 100 DM > 1000 DM 100 - 500 DM 500 - 1000 DM unknown

## 603 48 103 63 183

- The checking and savings account balance may prove to be important predictors of loan default status.

summary(credit$months_loan_duration)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 4.0 12.0 18.0 20.9 24.0 72.0

summary(credit$amount)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## 250 1366 2320 3271 3972 18420

table(credit$default)

##

## no yes

## 700 300

- The default vector indicates whether the loan applicant was unable to meet the agreed payment terms and went into default. Our model will identify applicants that are at high risk to default, allowing the bank to refuse credit requests.

Data preparation - creating random training and test datasets

The credit dataset is not randomly ordered, making the prior approach unwise. Suppose that the bank had sorted the data by the loan amount, with the largest loans at the end of the file. If we used the first 90 percent for training and the remaining 10 percent for testing, we would be training a model on only the small loans and testing the model on the big loans.

We’ll solve this problem by using a random sample of the credit data for training.

set.seed(123)

train_sample <- sample(1000,900)

# The resulting train_sample object is a vector of 900 random integers:

str(train_sample)

## int [1:900] 288 788 409 881 937 46 525 887 548 453 ...

# Split it into the 90 percent training and 10 percent test datasets:

credit_train <- credit[train_sample, ]

credit_test <- credit[-train_sample, ]

# we should have about 30 percent of defaulted loans in each of the datasets:

prop.table(table(credit_train$default))

##

## no yes

## 0.7033333 0.2966667

prop.table(table(credit_test$default))

##

## no yes

## 0.67 0.33

Step 3 - training a model on the data

library(C50)

## Warning: package 'C50' was built under R version 3.3.3

# The 17th column in credit_train is the default class variable, so we need to exclude it from the training data frame, but supply it as the target factor vector for classification.

credit_model <- C5.0(credit_train[-17], credit_train$default)

credit_model

##

## Call:

## C5.0.default(x = credit_train[-17], y = credit_train$default)

##

## Classification Tree

## Number of samples: 900

## Number of predictors: 16

##

## Tree size: 57

##

## Non-standard options: attempt to group attributes

- The tree is 57 decisions deep-quite a bit larger than the example trees we’ve considered so far!

summary(credit_model)

##

## Call:

## C5.0.default(x = credit_train[-17], y = credit_train$default)

##

##

## C5.0 [Release 2.07 GPL Edition] Fri Aug 11 21:59:19 2017

## -------------------------------

##

## Class specified by attribute `outcome'

##

## Read 900 cases (17 attributes) from undefined.data

##

## Decision tree:

##

## checking_balance in {> 200 DM,unknown}: no (412/50)

## checking_balance in {< 0 DM,1 - 200 DM}:

## :...credit_history in {perfect,very good}: yes (59/18)

## credit_history in {critical,good,poor}:

## :...months_loan_duration <= 22:

## :...credit_history = critical: no (72/14)

## : credit_history = poor:

## : :...dependents > 1: no (5)

## : : dependents <= 1:

## : : :...years_at_residence <= 3: yes (4/1)

## : : years_at_residence > 3: no (5/1)

## : credit_history = good:

## : :...savings_balance in {> 1000 DM,500 - 1000 DM}: no (15/1)

## : savings_balance = 100 - 500 DM:

## : :...other_credit = bank: yes (3)

## : : other_credit in {none,store}: no (9/2)

## : savings_balance = unknown:

## : :...other_credit = bank: yes (1)

## : : other_credit in {none,store}: no (21/8)

## : savings_balance = < 100 DM:

## : :...purpose in {business,car0,renovations}: no (8/2)

## : purpose = education:

## : :...checking_balance = < 0 DM: yes (4)

## : : checking_balance = 1 - 200 DM: no (1)

## : purpose = car:

## : :...employment_duration = > 7 years: yes (5)

## : : employment_duration = unemployed: no (4/1)

## : : employment_duration = < 1 year:

## : : :...years_at_residence <= 2: yes (5)

## : : : years_at_residence > 2: no (3/1)

## : : employment_duration = 1 - 4 years:

## : : :...years_at_residence <= 2: yes (2)

## : : : years_at_residence > 2: no (6/1)

## : : employment_duration = 4 - 7 years:

## : : :...amount <= 1680: yes (2)

## : : amount > 1680: no (3)

## : purpose = furniture/appliances:

## : :...job in {management,unskilled}: no (23/3)

## : job = unemployed: yes (1)

## : job = skilled:

## : :...months_loan_duration > 13: [S1]

## : months_loan_duration <= 13:

## : :...housing in {other,own}: no (23/4)

## : housing = rent:

## : :...percent_of_income <= 3: yes (3)

## : percent_of_income > 3: no (2)

## months_loan_duration > 22:

## :...savings_balance = > 1000 DM: no (2)

## savings_balance = 500 - 1000 DM: yes (4/1)

## savings_balance = 100 - 500 DM:

## :...credit_history in {critical,poor}: no (14/3)

## : credit_history = good:

## : :...other_credit = bank: no (1)

## : other_credit in {none,store}: yes (12/2)

## savings_balance = unknown:

## :...checking_balance = 1 - 200 DM: no (17)

## : checking_balance = < 0 DM:

## : :...credit_history = critical: no (1)

## : credit_history in {good,poor}: yes (12/3)

## savings_balance = < 100 DM:

## :...months_loan_duration > 47: yes (21/2)

## months_loan_duration <= 47:

## :...housing = other:

## :...percent_of_income <= 2: no (6)

## : percent_of_income > 2: yes (9/3)

## housing = rent:

## :...other_credit = bank: no (1)

## : other_credit in {none,store}: yes (16/3)

## housing = own:

## :...employment_duration = > 7 years: no (13/4)

## employment_duration = 4 - 7 years:

## :...job in {management,skilled,

## : : unemployed}: yes (9/1)

## : job = unskilled: no (1)

## employment_duration = unemployed:

## :...years_at_residence <= 2: yes (4)

## : years_at_residence > 2: no (3)

## employment_duration = 1 - 4 years:

## :...purpose in {business,car0,education}: yes (7/1)

## : purpose in {furniture/appliances,

## : : renovations}: no (7)

## : purpose = car:

## : :...years_at_residence <= 3: yes (3)

## : years_at_residence > 3: no (3)

## employment_duration = < 1 year:

## :...years_at_residence > 3: yes (5)

## years_at_residence <= 3:

## :...other_credit = bank: no (0)

## other_credit = store: yes (1)

## other_credit = none:

## :...checking_balance = 1 - 200 DM: no (8/2)

## checking_balance = < 0 DM:

## :...job in {management,skilled,

## : unemployed}: yes (2)

## job = unskilled: no (3/1)

##

## SubTree [S1]

##

## employment_duration in {< 1 year,4 - 7 years}: no (4)

## employment_duration in {> 7 years,1 - 4 years,unemployed}: yes (10)

##

##

## Evaluation on training data (900 cases):

##

## Decision Tree

## ----------------

## Size Errors

##

## 56 133(14.8%) <<

##

##

## (a) (b) <-classified as

## ---- ----

## 598 35 (a): class no

## 98 169 (b): class yes

##

##

## Attribute usage:

##

## 100.00% checking_balance

## 54.22% credit_history

## 47.67% months_loan_duration

## 38.11% savings_balance

## 14.33% purpose

## 14.33% housing

## 12.56% employment_duration

## 9.00% job

## 8.67% other_credit

## 6.33% years_at_residence

## 2.22% percent_of_income

## 1.56% dependents

## 0.56% amount

##

##

## Time: 0.0 secs

The first three lines could be represented in plain language as:

- If the checking account balance is unknown or greater than 200 DM, then classify as “not likely to default.” (412/50 indicates that of the 412 examples reaching the decision, 50 were incorrectly classified as not likely to default. In other words, 50 applicants actually defaulted, in spite of the model’s prediction to the contrary.)

- Otherwise, if the checking account balance is less than zero DM or between one and 200 DM.

- And the credit history is perfect or very good, then classify as “likely to default.”

The confusion matrix is a cross-tabulation that indicates the model’s incorrectly classified records in the training data:

- The model correctly classified all but 133 of the 900 training instances for an error rate of 14.8 percent.

- A total of 35 actual no values were incorrectly classified as yes (false positives), while 98 yes values were misclassified as no (false negatives).

- The error rate reported on training data may be overly optimistic

Step 4 - evaluating model performance

Create a vector of predicted class values, which we can compare to the

actual class values using the CrossTable() function in the gmodels

package. Set the prop.c and prop.r parameters to FALSE removes the

column and row percentages from the table. The remaining percentage

prop.t indicates the proportion of records in the cell out of the

total number of records:

credit_pred <- predict(credit_model, credit_test)

library(gmodels)

## Warning: package 'gmodels' was built under R version 3.3.3

CrossTable(credit_test$default, credit_pred, prop.chisq = FALSE, prop.c = FALSE, prop.r = FALSE,

dnn = c('actual default', 'predicted default'))

##

##

## Cell Contents

## |-------------------------|

## | N |

## | N / Table Total |

## |-------------------------|

##

##

## Total Observations in Table: 100

##

##

## | predicted default

## actual default | no | yes | Row Total |

## ---------------|-----------|-----------|-----------|

## no | 59 | 8 | 67 |

## | 0.590 | 0.080 | |

## ---------------|-----------|-----------|-----------|

## yes | 19 | 14 | 33 |

## | 0.190 | 0.140 | |

## ---------------|-----------|-----------|-----------|

## Column Total | 78 | 22 | 100 |

## ---------------|-----------|-----------|-----------|

##

##

- Out of the 100 test loan application records, our model correctly predicted that 59 did not default and 14 did default, resulting in an accuracy of 73 percent and an error rate of 27 percent. This is somewhat worse than its performance on the training data, but not unexpected, given that a model’s performance is often worse on unseen data.

- Also note that the model only correctly predicted 14 of the 33 actual loan defaults in the test data, or 42 percent. Unfortunately, this type of error is a potentially very costly mistake, as the bank loses money on each default.

Step 5 - improving model performance

Boosting the accuracy of decision trees

Add an additional trials parameter indicating the number of separate decision trees to use in the boosted team. The trials parameter sets an upper limit; the algorithm will stop adding trees if it recognizes that additional trials do not seem to be improving the accuracy.

credit_boost10 <- C5.0(credit_train[-17], credit_train$default, trials = 10)

#Across the 10 iterations, our tree size shrunk.

credit_boost10

##

## Call:

## C5.0.default(x = credit_train[-17], y = credit_train$default, trials = 10)

##

## Classification Tree

## Number of samples: 900

## Number of predictors: 16

##

## Number of boosting iterations: 10

## Average tree size: 47.5

##

## Non-standard options: attempt to group attributes

summary(credit_boost10)

##

## Call:

## C5.0.default(x = credit_train[-17], y = credit_train$default, trials = 10)

##

##

## C5.0 [Release 2.07 GPL Edition] Fri Aug 11 21:59:19 2017

## -------------------------------

##

## Class specified by attribute `outcome'

##

## Read 900 cases (17 attributes) from undefined.data

##

## ----- Trial 0: -----

##

## Decision tree:

##

## checking_balance in {> 200 DM,unknown}: no (412/50)

## checking_balance in {< 0 DM,1 - 200 DM}:

## :...credit_history in {perfect,very good}: yes (59/18)

## credit_history in {critical,good,poor}:

## :...months_loan_duration <= 22:

## :...credit_history = critical: no (72/14)

## : credit_history = poor:

## : :...dependents > 1: no (5)

## : : dependents <= 1:

## : : :...years_at_residence <= 3: yes (4/1)

## : : years_at_residence > 3: no (5/1)

## : credit_history = good:

## : :...savings_balance in {> 1000 DM,500 - 1000 DM}: no (15/1)

## : savings_balance = 100 - 500 DM:

## : :...other_credit = bank: yes (3)

## : : other_credit in {none,store}: no (9/2)

## : savings_balance = unknown:

## : :...other_credit = bank: yes (1)

## : : other_credit in {none,store}: no (21/8)

## : savings_balance = < 100 DM:

## : :...purpose in {business,car0,renovations}: no (8/2)

## : purpose = education:

## : :...checking_balance = < 0 DM: yes (4)

## : : checking_balance = 1 - 200 DM: no (1)

## : purpose = car:

## : :...employment_duration = > 7 years: yes (5)

## : : employment_duration = unemployed: no (4/1)

## : : employment_duration = < 1 year:

## : : :...years_at_residence <= 2: yes (5)

## : : : years_at_residence > 2: no (3/1)

## : : employment_duration = 1 - 4 years:

## : : :...years_at_residence <= 2: yes (2)

## : : : years_at_residence > 2: no (6/1)

## : : employment_duration = 4 - 7 years:

## : : :...amount <= 1680: yes (2)

## : : amount > 1680: no (3)

## : purpose = furniture/appliances:

## : :...job in {management,unskilled}: no (23/3)

## : job = unemployed: yes (1)

## : job = skilled:

## : :...months_loan_duration > 13: [S1]

## : months_loan_duration <= 13:

## : :...housing in {other,own}: no (23/4)

## : housing = rent:

## : :...percent_of_income <= 3: yes (3)

## : percent_of_income > 3: no (2)

## months_loan_duration > 22:

## :...savings_balance = > 1000 DM: no (2)

## savings_balance = 500 - 1000 DM: yes (4/1)

## savings_balance = 100 - 500 DM:

## :...credit_history in {critical,poor}: no (14/3)

## : credit_history = good:

## : :...other_credit = bank: no (1)

## : other_credit in {none,store}: yes (12/2)

## savings_balance = unknown:

## :...checking_balance = 1 - 200 DM: no (17)

## : checking_balance = < 0 DM:

## : :...credit_history = critical: no (1)

## : credit_history in {good,poor}: yes (12/3)

## savings_balance = < 100 DM:

## :...months_loan_duration > 47: yes (21/2)

## months_loan_duration <= 47:

## :...housing = other:

## :...percent_of_income <= 2: no (6)

## : percent_of_income > 2: yes (9/3)

## housing = rent:

## :...other_credit = bank: no (1)

## : other_credit in {none,store}: yes (16/3)

## housing = own:

## :...employment_duration = > 7 years: no (13/4)

## employment_duration = 4 - 7 years:

## :...job in {management,skilled,

## : : unemployed}: yes (9/1)

## : job = unskilled: no (1)

## employment_duration = unemployed:

## :...years_at_residence <= 2: yes (4)

## : years_at_residence > 2: no (3)

## employment_duration = 1 - 4 years:

## :...purpose in {business,car0,education}: yes (7/1)

## : purpose in {furniture/appliances,

## : : renovations}: no (7)

## : purpose = car:

## : :...years_at_residence <= 3: yes (3)

## : years_at_residence > 3: no (3)

## employment_duration = < 1 year:

## :...years_at_residence > 3: yes (5)

## years_at_residence <= 3:

## :...other_credit = bank: no (0)

## other_credit = store: yes (1)

## other_credit = none:

## :...checking_balance = 1 - 200 DM: no (8/2)

## checking_balance = < 0 DM:

## :...job in {management,skilled,

## : unemployed}: yes (2)

## job = unskilled: no (3/1)

##

## SubTree [S1]

##

## employment_duration in {< 1 year,4 - 7 years}: no (4)

## employment_duration in {> 7 years,1 - 4 years,unemployed}: yes (10)

##

## ----- Trial 1: -----

##

## Decision tree:

##

## checking_balance = unknown:

## :...other_credit in {bank,store}:

## : :...purpose in {business,education,renovations}: yes (19.5/6.3)

## : : purpose in {car0,furniture/appliances}: no (24.8/6.6)

## : : purpose = car:

## : : :...dependents <= 1: yes (20.1/4.8)

## : : dependents > 1: no (2.4)

## : other_credit = none:

## : :...credit_history in {critical,perfect,very good}: no (102.8/4.4)

## : credit_history = good:

## : :...existing_loans_count <= 1: no (112.7/17.5)

## : : existing_loans_count > 1: yes (18.9/7.9)

## : credit_history = poor:

## : :...years_at_residence <= 1: yes (4.4)

## : years_at_residence > 1:

## : :...percent_of_income <= 3: no (11.9)

## : percent_of_income > 3: yes (14.3/5.6)

## checking_balance in {< 0 DM,> 200 DM,1 - 200 DM}:

## :...savings_balance in {> 1000 DM,500 - 1000 DM}: no (42.9/11.3)

## savings_balance = unknown:

## :...credit_history in {perfect,poor}: no (8.5)

## : credit_history in {critical,good,very good}:

## : :...employment_duration in {< 1 year,> 7 years,4 - 7 years,

## : : unemployed}: no (52.3/17.3)

## : employment_duration = 1 - 4 years: yes (19.7/5.6)

## savings_balance = 100 - 500 DM:

## :...existing_loans_count > 3: yes (3)

## : existing_loans_count <= 3:

## : :...credit_history in {critical,poor,very good}: no (24.6/7.6)

## : credit_history = perfect: yes (2.4)

## : credit_history = good:

## : :...months_loan_duration <= 27: no (23.7/10.5)

## : months_loan_duration > 27: yes (5.6)

## savings_balance = < 100 DM:

## :...months_loan_duration > 42: yes (28/5.2)

## months_loan_duration <= 42:

## :...percent_of_income <= 2:

## :...employment_duration in {1 - 4 years,4 - 7 years,

## : : unemployed}: no (86.2/23.8)

## : employment_duration in {< 1 year,> 7 years}:

## : :...housing = other: no (4.8/1.6)

## : housing = rent: yes (10.7/2.4)

## : housing = own:

## : :...phone = yes: yes (12.9/4)

## : phone = no:

## : :...percent_of_income <= 1: no (7.1/0.8)

## : percent_of_income > 1: yes (17.5/7.1)

## percent_of_income > 2:

## :...years_at_residence <= 1: no (31.6/8.5)

## years_at_residence > 1:

## :...credit_history in {perfect,poor}: yes (20.9/1.6)

## credit_history in {critical,good,very good}:

## :...job = skilled: yes (95/34.7)

## job = unemployed: no (1.6)

## job = management:

## :...amount <= 11590: no (23.8/7)

## : amount > 11590: yes (3.8)

## job = unskilled:

## :...checking_balance in {< 0 DM,

## : > 200 DM}: yes (23.8/9.5)

## checking_balance = 1 - 200 DM: no (17.9/6.2)

##

## ----- Trial 2: -----

##

## Decision tree:

##

## checking_balance = unknown:

## :...other_credit = bank:

## : :...existing_loans_count > 2: no (3.3)

## : : existing_loans_count <= 2:

## : : :...months_loan_duration <= 8: no (4)

## : : months_loan_duration > 8: yes (43/16.6)

## : other_credit in {none,store}:

## : :...employment_duration in {< 1 year,unemployed}:

## : :...purpose in {business,renovations}: yes (6.4)

## : : purpose in {car,car0,education}: no (13.2)

## : : purpose = furniture/appliances:

## : : :...amount <= 4594: no (22.5/7.3)

## : : amount > 4594: yes (9.1)

## : employment_duration in {> 7 years,1 - 4 years,4 - 7 years}:

## : :...percent_of_income <= 3: no (92.7/3.6)

## : percent_of_income > 3:

## : :...age > 30: no (73.6/5.5)

## : age <= 30:

## : :...job in {management,unemployed,unskilled}: yes (14/4)

## : job = skilled:

## : :...credit_history = very good: no (0)

## : credit_history = poor: yes (3.6)

## : credit_history in {critical,good,perfect}:

## : :...age <= 29: no (20.4/4.6)

## : age > 29: yes (2.7)

## checking_balance in {< 0 DM,> 200 DM,1 - 200 DM}:

## :...housing = other:

## :...dependents > 1: yes (28.3/7.6)

## : dependents <= 1:

## : :...employment_duration in {< 1 year,4 - 7 years,

## : : unemployed}: no (22.9/4.5)

## : employment_duration in {> 7 years,1 - 4 years}: yes (29.6/10.5)

## housing = rent:

## :...credit_history = perfect: yes (5.3)

## : credit_history = poor: no (7.1/0.7)

## : credit_history in {critical,good,very good}:

## : :...employment_duration = < 1 year: yes (28.3/9.3)

## : employment_duration in {> 7 years,4 - 7 years,

## : : unemployed}: no (33.9/12.3)

## : employment_duration = 1 - 4 years:

## : :...checking_balance = > 200 DM: no (2)

## : checking_balance in {< 0 DM,1 - 200 DM}:

## : :...years_at_residence <= 3: no (10.3/3.8)

## : years_at_residence > 3: yes (20.4/3.1)

## housing = own:

## :...job in {management,unemployed}: yes (55.8/19.8)

## job in {skilled,unskilled}:

## :...months_loan_duration <= 7: no (25.3/2)

## months_loan_duration > 7:

## :...years_at_residence > 3: no (92.2/29.6)

## years_at_residence <= 3:

## :...purpose = renovations: yes (7/1.3)

## purpose in {business,car0,education}: no (32.2/5.3)

## purpose = car:

## :...months_loan_duration > 40: no (7.2/0.7)

## : months_loan_duration <= 40:

## : :...amount <= 947: yes (12.9)

## : amount > 947:

## : :...months_loan_duration <= 16: no (23.2/8.5)

## : months_loan_duration > 16: [S1]

## purpose = furniture/appliances:

## :...savings_balance in {> 1000 DM,unknown}: no (15.4/3.2)

## savings_balance in {100 - 500 DM,

## : 500 - 1000 DM}: yes (14.6/4.5)

## savings_balance = < 100 DM:

## :...months_loan_duration > 36: yes (7.1)

## months_loan_duration <= 36:

## :...existing_loans_count > 1: no (14.1/4.3)

## existing_loans_count <= 1: [S2]

##

## SubTree [S1]

##

## savings_balance in {< 100 DM,> 1000 DM,500 - 1000 DM,unknown}: yes (22.5/2.7)

## savings_balance = 100 - 500 DM: no (4.5/0.7)

##

## SubTree [S2]

##

## checking_balance = < 0 DM: no (22.4/9.1)

## checking_balance in {> 200 DM,1 - 200 DM}: yes (46.7/20)

##

## ----- Trial 3: -----

##

## Decision tree:

##

## checking_balance in {> 200 DM,unknown}:

## :...employment_duration = > 7 years: no (98.9/17.1)

## : employment_duration = unemployed: yes (16/6.7)

## : employment_duration = < 1 year:

## : :...amount <= 1333: no (11.7)

## : : amount > 1333:

## : : :...amount <= 6681: no (38.2/16.3)

## : : amount > 6681: yes (5.3)

## : employment_duration = 4 - 7 years:

## : :...checking_balance = > 200 DM: yes (9.6/3.6)

## : : checking_balance = unknown:

## : : :...age <= 22: yes (6.5/1.6)

## : : age > 22: no (42.6/1.5)

## : employment_duration = 1 - 4 years:

## : :...percent_of_income <= 1: no (20.6/1.5)

## : percent_of_income > 1:

## : :...job in {skilled,unemployed}: no (64.9/17.6)

## : job in {management,unskilled}:

## : :...existing_loans_count > 2: yes (2.4)

## : existing_loans_count <= 2:

## : :...age <= 34: yes (26.4/10.7)

## : age > 34: no (10.5)

## checking_balance in {< 0 DM,1 - 200 DM}:

## :...savings_balance in {> 1000 DM,500 - 1000 DM}: no (35.8/12)

## savings_balance = 100 - 500 DM:

## :...amount <= 1285: yes (12.8/0.5)

## : amount > 1285:

## : :...existing_loans_count <= 1: no (27/9.2)

## : existing_loans_count > 1: yes (15.8/4.9)

## savings_balance = unknown:

## :...credit_history in {critical,perfect,poor}: no (15.5)

## : credit_history in {good,very good}:

## : :...age > 56: no (4.5)

## : age <= 56:

## : :...months_loan_duration <= 18: yes (24.5/5.6)

## : months_loan_duration > 18: no (28.4/12.3)

## savings_balance = < 100 DM:

## :...months_loan_duration <= 11:

## :...job = management: yes (13.7/4.9)

## : job in {skilled,unemployed,unskilled}: no (45.9/10)

## months_loan_duration > 11:

## :...percent_of_income <= 1:

## :...credit_history in {critical,poor,very good}: no (11.1)

## : credit_history in {good,perfect}: yes (24.4/11)

## percent_of_income > 1:

## :...job = unemployed: yes (7/3.1)

## job = management:

## :...years_at_residence <= 1: no (6.6)

## : years_at_residence > 1:

## : :...checking_balance = < 0 DM: no (23.1/7)

## : checking_balance = 1 - 200 DM: yes (15.8/4)

## job = unskilled:

## :...housing in {other,rent}: yes (12.2/2.2)

## : housing = own:

## : :...purpose = car: yes (18.1/3.9)

## : purpose in {business,car0,education,

## : furniture/appliances,

## : renovations}: no (32.1/11.1)

## job = skilled:

## :...checking_balance = < 0 DM:

## :...credit_history in {poor,very good}: yes (16.6)

## : credit_history in {critical,good,perfect}:

## : :...purpose in {business,car0,education,

## : : renovations}: yes (10.2/1.5)

## : purpose = car:

## : :...age <= 51: yes (34.6/8.1)

## : : age > 51: no (4.4)

## : purpose = furniture/appliances:

## : :...years_at_residence <= 1: no (4.4)

## : years_at_residence > 1:

## : :...other_credit = bank: yes (2.4)

## : other_credit = store: no (0.5)

## : other_credit = none:

## : :...amount <= 1743: no (11.5/2.4)

## : amount > 1743: yes (29/6.6)

## checking_balance = 1 - 200 DM:

## :...months_loan_duration > 36: yes (6.5)

## months_loan_duration <= 36:

## :...other_credit in {bank,store}: yes (8/1.5)

## other_credit = none:

## :...dependents > 1: yes (7.4/3.1)

## dependents <= 1:

## :...percent_of_income <= 2: no (12.7/1.1)

## percent_of_income > 2: [S1]

##

## SubTree [S1]

##

## purpose in {business,renovations}: yes (3.9)

## purpose in {car,car0,education,furniture/appliances}: no (19.8/6.1)

##

## ----- Trial 4: -----

##

## Decision tree:

##

## checking_balance in {> 200 DM,unknown}:

## :...other_credit = store: no (20.6/9.6)

## : other_credit = none:

## : :...employment_duration in {> 7 years,1 - 4 years,4 - 7 years,

## : : : unemployed}: no (211.3/45.7)

## : : employment_duration = < 1 year:

## : : :...amount <= 1333: no (8.8)

## : : amount > 1333:

## : : :...purpose in {business,car0,education,furniture/appliances,

## : : : renovations}: yes (32.9/8.1)

## : : purpose = car: no (4.9)

## : other_credit = bank:

## : :...age > 44: no (14.4/1.2)

## : age <= 44:

## : :...years_at_residence <= 1: no (5)

## : years_at_residence > 1:

## : :...housing = rent: yes (4.3)

## : housing in {other,own}:

## : :...job = unemployed: yes (0)

## : job = management: no (4)

## : job in {skilled,unskilled}:

## : :...age <= 26: no (3.7)

## : age > 26:

## : :...savings_balance in {< 100 DM,500 - 1000 DM,

## : : unknown}: yes (30.6/7.4)

## : savings_balance in {> 1000 DM,

## : 100 - 500 DM}: no (4)

## checking_balance in {< 0 DM,1 - 200 DM}:

## :...credit_history = perfect:

## :...housing in {other,rent}: yes (7.8)

## : housing = own: no (20.5/9)

## credit_history = poor:

## :...checking_balance = < 0 DM: yes (10.4/2.2)

## : checking_balance = 1 - 200 DM:

## : :...other_credit in {bank,none}: no (24/4.3)

## : other_credit = store: yes (5.8/1.2)

## credit_history = very good:

## :...age <= 23: no (5.7)

## : age > 23:

## : :...months_loan_duration <= 27: yes (28.4/3.7)

## : months_loan_duration > 27: no (6.9/2)

## credit_history = critical:

## :...years_at_residence <= 1: no (6.7)

## : years_at_residence > 1:

## : :...purpose in {business,car,car0,renovations}: no (62.2/21.9)

## : purpose = education: yes (7.9/0.9)

## : purpose = furniture/appliances:

## : :...phone = yes: no (14.5/2.8)

## : phone = no:

## : :...amount <= 1175: no (5.2)

## : amount > 1175: yes (30.1/7.6)

## credit_history = good:

## :...savings_balance in {> 1000 DM,500 - 1000 DM}: no (15.7/4.7)

## savings_balance = 100 - 500 DM: yes (32.1/11.7)

## savings_balance = unknown:

## :...job = unskilled: no (4.4)

## : job in {management,skilled,unemployed}:

## : :...checking_balance = < 0 DM: yes (27.8/6)

## : checking_balance = 1 - 200 DM: no (26.8/10.4)

## savings_balance = < 100 DM:

## :...dependents > 1:

## :...existing_loans_count > 1: no (2.6/0.4)

## : existing_loans_count <= 1:

## : :...years_at_residence <= 2: yes (10.2/2.9)

## : years_at_residence > 2: no (20.4/5.9)

## dependents <= 1:

## :...purpose in {business,car0}: no (9.7/2.5)

## purpose in {education,renovations}: yes (13/5.1)

## purpose = car:

## :...employment_duration in {< 1 year,> 7 years,

## : : 4 - 7 years}: yes (32/8.3)

## : employment_duration in {1 - 4 years,

## : unemployed}: no (24.9/9)

## purpose = furniture/appliances:

## :...months_loan_duration > 39: yes (4.8)

## months_loan_duration <= 39:

## :...phone = yes: yes (21.9/9.2)

## phone = no:

## :...employment_duration in {< 1 year,> 7 years,

## : 4 - 7 years}: no (34.1/8.1)

## employment_duration = unemployed: yes (3.3/0.4)

## employment_duration = 1 - 4 years:

## :...percent_of_income <= 1: yes (3.8)

## percent_of_income > 1:

## :...months_loan_duration > 21: no (4.9/0.4)

## months_loan_duration <= 21:

## :...years_at_residence <= 3: no (20.9/8.8)

## years_at_residence > 3: yes (5.8)

##

## ----- Trial 5: -----

##

## Decision tree:

##

## checking_balance = unknown:

## :...other_credit = store: yes (16.9/7.5)

## : other_credit = bank:

## : :...housing = other: no (8.3/1.8)

## : : housing = rent: yes (4.4/0.8)

## : : housing = own:

## : : :...phone = no: no (26.9/9.7)

## : : phone = yes: yes (12.1/5)

## : other_credit = none:

## : :...credit_history in {critical,perfect,very good}: no (60.4/5.1)

## : credit_history in {good,poor}:

## : :...purpose in {business,car,car0,education}: no (53.6/12.8)

## : purpose = renovations: yes (7.3/1.1)

## : purpose = furniture/appliances:

## : :...job = unemployed: no (0)

## : job in {management,unskilled}: yes (19.2/7)

## : job = skilled:

## : :...phone = yes: no (14.6/1.8)

## : phone = no:

## : :...age > 32: no (9.2)

## : age <= 32:

## : :...employment_duration = 1 - 4 years: no (4.1)

## : employment_duration in {< 1 year,> 7 years,

## : : 4 - 7 years,unemployed}:

## : :...savings_balance in {< 100 DM,

## : : 100 - 500 DM}: yes (20.5/3)

## : savings_balance in {> 1000 DM,500 - 1000 DM,

## : unknown}: no (3.4)

## checking_balance in {< 0 DM,> 200 DM,1 - 200 DM}:

## :...percent_of_income <= 2:

## :...amount > 11054: yes (14.2/1.2)

## : amount <= 11054:

## : :...other_credit = bank: no (32.3/9.7)

## : other_credit = store: yes (8.9/2.6)

## : other_credit = none:

## : :...purpose in {business,renovations}: yes (20.3/9.1)

## : purpose in {car0,education}: no (8.4/3.7)

## : purpose = car:

## : :...savings_balance in {< 100 DM,> 1000 DM,500 - 1000 DM,

## : : : unknown}: no (46.6/7.9)

## : : savings_balance = 100 - 500 DM: yes (13.8/3.3)

## : purpose = furniture/appliances:

## : :...employment_duration in {> 7 years,

## : : 4 - 7 years}: no (18.2/2.6)

## : employment_duration in {1 - 4 years,

## : : unemployed}: yes (50.8/19.5)

## : employment_duration = < 1 year:

## : :...job in {management,skilled,unemployed}: no (16.3/2.9)

## : job = unskilled: yes (6/1.6)

## percent_of_income > 2:

## :...years_at_residence <= 1:

## :...other_credit in {bank,store}: no (7.6)

## : other_credit = none:

## : :...months_loan_duration > 42: no (2.9)

## : months_loan_duration <= 42:

## : :...age <= 36: no (26.6/8.4)

## : age > 36: yes (5.3)

## years_at_residence > 1:

## :...job = unemployed: no (5.2)

## job in {management,skilled,unskilled}:

## :...credit_history = perfect: yes (10.9)

## credit_history in {critical,good,poor,very good}:

## :...employment_duration = < 1 year:

## :...checking_balance = > 200 DM: no (2.7)

## : checking_balance in {< 0 DM,1 - 200 DM}:

## : :...months_loan_duration > 21: yes (23.4/0.7)

## : months_loan_duration <= 21:

## : :...amount <= 1928: yes (18.4/4.4)

## : amount > 1928: no (4.5)

## employment_duration in {> 7 years,1 - 4 years,4 - 7 years,

## : unemployed}:

## :...months_loan_duration <= 11:

## :...age > 47: no (12.2)

## : age <= 47:

## : :...purpose in {business,car,car0,

## : : furniture/appliances,

## : : renovations}: no (25/9.2)

## : purpose = education: yes (3.5)

## months_loan_duration > 11:

## :...savings_balance in {> 1000 DM,100 - 500 DM}:

## :...age <= 58: no (22.7/3.4)

## : age > 58: yes (4.4)

## savings_balance in {< 100 DM,500 - 1000 DM,unknown}:

## :...years_at_residence <= 2: yes (76.1/22.8)

## years_at_residence > 2:

## :...purpose in {business,car0,

## : education}: yes (24.7/7.1)

## purpose = renovations: no (1.1)

## purpose = furniture/appliances: [S1]

## purpose = car:

## :...amount <= 1388: yes (17.8/2.2)

## amount > 1388:

## :...housing = own: no (10.9)

## housing in {other,rent}: [S2]

##

## SubTree [S1]

##

## employment_duration = unemployed: no (4.4)

## employment_duration in {> 7 years,1 - 4 years,4 - 7 years}:

## :...checking_balance = < 0 DM: yes (35.6/12.4)

## checking_balance in {> 200 DM,1 - 200 DM}: no (29/10.5)

##

## SubTree [S2]

##

## savings_balance in {< 100 DM,500 - 1000 DM}: yes (21.4/6.4)

## savings_balance = unknown: no (6.8/1.5)

##

## ----- Trial 6: -----

##

## Decision tree:

##

## checking_balance in {> 200 DM,unknown}:

## :...purpose = car0: no (2.2)

## : purpose = renovations: yes (8.4/3.3)

## : purpose = education:

## : :...age <= 44: yes (19.8/7.7)

## : : age > 44: no (4.4)

## : purpose = business:

## : :...existing_loans_count > 2: yes (3.3)

## : : existing_loans_count <= 2:

## : : :...amount <= 1823: no (8.1)

## : : amount > 1823:

## : : :...percent_of_income <= 3: no (12.1/3.3)

## : : percent_of_income > 3: yes (13.2/3.4)

## : purpose = car:

## : :...job in {management,unemployed}: no (20.8/1.6)

## : : job = unskilled:

## : : :...years_at_residence <= 3: no (11/1.3)

## : : : years_at_residence > 3: yes (14.5/3.2)

## : : job = skilled:

## : : :...other_credit in {bank,store}: yes (17.6/4.9)

## : : other_credit = none:

## : : :...existing_loans_count <= 2: no (24.6)

## : : existing_loans_count > 2: yes (2.4/0.3)

## : purpose = furniture/appliances:

## : :...age > 44: no (22.7)

## : age <= 44:

## : :...job = unemployed: no (0)

## : job = unskilled:

## : :...existing_loans_count <= 1: yes (20.9/5.6)

## : : existing_loans_count > 1: no (4.5)

## : job in {management,skilled}:

## : :...dependents > 1: no (6.6)

## : dependents <= 1:

## : :...existing_loans_count <= 1:

## : :...savings_balance in {> 1000 DM,100 - 500 DM,

## : : : 500 - 1000 DM,

## : : : unknown}: no (16.9)

## : : savings_balance = < 100 DM:

## : : :...age <= 22: yes (8.5/1.3)

## : : age > 22: no (43.1/8.8)

## : existing_loans_count > 1:

## : :...housing in {other,rent}: yes (9.9/2.1)

## : housing = own:

## : :...credit_history in {critical,poor,

## : : very good}: no (18.6/1.6)

## : credit_history in {good,perfect}: yes (14.9/4.3)

## checking_balance in {< 0 DM,1 - 200 DM}:

## :...credit_history = perfect: yes (28.1/9.6)

## credit_history = very good:

## :...age <= 23: no (5.5)

## : age > 23: yes (30/8.1)

## credit_history = poor:

## :...percent_of_income <= 1: no (6.5)

## : percent_of_income > 1:

## : :...savings_balance in {500 - 1000 DM,unknown}: no (6.4)

## : savings_balance in {< 100 DM,> 1000 DM,100 - 500 DM}:

## : :...dependents <= 1: yes (25.1/8)

## : dependents > 1: no (5/0.9)

## credit_history = critical:

## :...savings_balance = unknown: no (8.4)

## : savings_balance in {< 100 DM,> 1000 DM,100 - 500 DM,500 - 1000 DM}:

## : :...other_credit = bank: yes (16.2/4.3)

## : other_credit = store: no (3.7/0.9)

## : other_credit = none:

## : :...savings_balance in {> 1000 DM,500 - 1000 DM}: yes (7.3/2.3)

## : savings_balance = 100 - 500 DM: no (5.9)

## : savings_balance = < 100 DM:

## : :...purpose = business: no (4.5/2.2)

## : purpose in {car0,education,renovations}: yes (8.5/2.2)

## : purpose = car:

## : :...age <= 29: yes (6.9)

## : : age > 29: no (25.6/6.9)

## : purpose = furniture/appliances:

## : :...months_loan_duration <= 36: no (38.4/10.9)

## : months_loan_duration > 36: yes (3.8)

## credit_history = good:

## :...amount > 8086: yes (24/3.8)

## amount <= 8086:

## :...phone = yes:

## :...age <= 28: yes (23.9/7.5)

## : age > 28: no (69.4/17.9)

## phone = no:

## :...other_credit in {bank,store}: yes (25.1/7.2)

## other_credit = none:

## :...percent_of_income <= 2:

## :...job in {management,unemployed,unskilled}: no (15.6/2.7)

## : job = skilled:

## : :...amount <= 1386: yes (9.9/1)

## : amount > 1386:

## : :...age <= 24: yes (13.4/4.6)

## : age > 24: no (27.8/3.1)

## percent_of_income > 2:

## :...checking_balance = < 0 DM: yes (62.5/21.4)

## checking_balance = 1 - 200 DM:

## :...months_loan_duration > 42: yes (4.9)

## months_loan_duration <= 42:

## :...existing_loans_count > 1: no (5)

## existing_loans_count <= 1:

## :...age <= 35: no (39.4/13.2)

## age > 35: yes (14.7/4.2)

##

## ----- Trial 7: -----

##

## Decision tree:

##

## checking_balance = unknown:

## :...employment_duration in {> 7 years,4 - 7 years}: no (101.1/20.4)

## : employment_duration = unemployed: yes (16.6/8)

## : employment_duration = < 1 year:

## : :...amount <= 4594: no (30/5.7)

## : : amount > 4594: yes (10.6/0.3)

## : employment_duration = 1 - 4 years:

## : :...dependents > 1: no (8)

## : dependents <= 1:

## : :...months_loan_duration <= 16: no (32.8/5.3)

## : months_loan_duration > 16:

## : :...existing_loans_count > 2: yes (2.7)

## : existing_loans_count <= 2:

## : :...percent_of_income <= 3: no (20.9/5.9)

## : percent_of_income > 3:

## : :...purpose in {business,car0,education}: yes (10.8)

## : purpose in {car,furniture/appliances,

## : renovations}: no (19.7/7.5)

## checking_balance in {< 0 DM,> 200 DM,1 - 200 DM}:

## :...purpose in {car0,education,renovations}: no (67.2/29.2)

## purpose = business:

## :...age > 46: yes (5.2)

## : age <= 46:

## : :...months_loan_duration <= 18: no (17.5)

## : months_loan_duration > 18:

## : :...other_credit in {bank,store}: no (10/0.5)

## : other_credit = none:

## : :...employment_duration in {> 7 years,

## : : unemployed}: yes (6.6)

## : employment_duration in {< 1 year,1 - 4 years,4 - 7 years}:

## : :...age <= 25: yes (4)

## : age > 25: no (19.2/5.6)

## purpose = car:

## :...amount <= 1297: yes (52.4/12.9)

## : amount > 1297:

## : :...percent_of_income <= 2:

## : :...phone = no: no (32.7/6.1)

## : : phone = yes:

## : : :...years_at_residence <= 3: no (20/4.9)

## : : years_at_residence > 3: yes (14.7/3.8)

## : percent_of_income > 2:

## : :...percent_of_income <= 3: yes (33.1/11.3)

## : percent_of_income > 3:

## : :...months_loan_duration <= 18: no (18.2/1.6)

## : months_loan_duration > 18:

## : :...existing_loans_count <= 1: no (19.5/7.2)

## : existing_loans_count > 1: yes (13.8/1)

## purpose = furniture/appliances:

## :...savings_balance = > 1000 DM: no (5.2)

## savings_balance = 100 - 500 DM: yes (18.6/6)

## savings_balance in {< 100 DM,500 - 1000 DM,unknown}:

## :...existing_loans_count > 1:

## :...existing_loans_count > 2: no (3.6)

## : existing_loans_count <= 2:

## : :...housing = other: yes (3.3)

## : housing in {own,rent}:

## : :...savings_balance = 500 - 1000 DM: yes (3.5/1)

## : savings_balance = unknown: no (6.9)

## : savings_balance = < 100 DM:

## : :...age > 54: yes (2.1)

## : age <= 54: [S1]

## existing_loans_count <= 1:

## :...credit_history in {critical,perfect}: yes (20.3/7.6)

## credit_history in {poor,very good}: no (20.8/9.5)

## credit_history = good:

## :...months_loan_duration <= 7: no (11.4)

## months_loan_duration > 7:

## :...other_credit = bank: no (14.2/4.6)

## other_credit = store: yes (11.7/3.9)

## other_credit = none:

## :...percent_of_income <= 1: no (20.5/5.2)

## percent_of_income > 1:

## :...amount > 6078: yes (10.9/1.1)

## amount <= 6078:

## :...dependents > 1: yes (8.7/2.5)

## dependents <= 1: [S2]

##

## SubTree [S1]

##

## employment_duration in {< 1 year,4 - 7 years}: yes (15/2.5)

## employment_duration in {> 7 years,1 - 4 years,unemployed}: no (25.7/2.9)

##

## SubTree [S2]

##

## employment_duration = > 7 years: no (17.9/2.5)

## employment_duration in {< 1 year,1 - 4 years,4 - 7 years,unemployed}:

## :...job = management: no (6.6)

## job = unemployed: yes (1.1)

## job in {skilled,unskilled}:

## :...years_at_residence <= 1: no (11.8/1.8)

## years_at_residence > 1:

## :...checking_balance = > 200 DM: no (14.7/6.3)

## checking_balance = 1 - 200 DM: yes (25.1/8.8)

## checking_balance = < 0 DM:

## :...months_loan_duration <= 16: no (13.8/3.4)

## months_loan_duration > 16: yes (19.1/5.5)

##

## ----- Trial 8: -----

##

## Decision tree:

##

## checking_balance in {< 0 DM,1 - 200 DM}:

## :...credit_history = perfect:

## : :...housing in {other,rent}: yes (8.3)

## : : housing = own:

## : : :...age <= 34: no (16.6/4.7)

## : : age > 34: yes (5.8)

## : credit_history = poor:

## : :...checking_balance = < 0 DM: yes (12/2.7)

## : : checking_balance = 1 - 200 DM:

## : : :...housing = rent: no (8.6)

## : : housing in {other,own}:

## : : :...amount <= 2279: yes (6.8/0.6)

## : : amount > 2279: no (20/5.7)

## : credit_history = very good:

## : :...existing_loans_count > 1: yes (2.5)

## : : existing_loans_count <= 1:

## : : :...age <= 23: no (3.7)

## : : age > 23:

## : : :...amount <= 8386: yes (32.9/8.1)

## : : amount > 8386: no (2.5)

## : credit_history = critical:

## : :...years_at_residence <= 1: no (8)

## : : years_at_residence > 1:

## : : :...savings_balance in {> 1000 DM,100 - 500 DM,500 - 1000 DM,

## : : : unknown}: no (25.5/5.7)

## : : savings_balance = < 100 DM:

## : : :...age > 61: no (6)

## : : age <= 61:

## : : :...existing_loans_count > 2: no (10.7/2.4)

## : : existing_loans_count <= 2:

## : : :...age > 56: yes (5.4)

## : : age <= 56:

## : : :...amount > 2483: yes (34.1/8.9)

## : : amount <= 2483:

## : : :...purpose in {business,education}: yes (4.4)

## : : purpose in {car,car0,furniture/appliances,

## : : renovations}: no (41.4/10.8)

## : credit_history = good:

## : :...amount > 8086: yes (26.6/4.8)

## : amount <= 8086:

## : :...savings_balance in {> 1000 DM,500 - 1000 DM}: no (17.5/5.1)

## : savings_balance = 100 - 500 DM:

## : :...months_loan_duration <= 27: no (21.3/7.1)

## : : months_loan_duration > 27: yes (5.1)

## : savings_balance = unknown:

## : :...age <= 56: yes (44.7/16.9)

## : : age > 56: no (4.4)

## : savings_balance = < 100 DM:

## : :...job = unemployed: yes (0.9)

## : job = management:

## : :...employment_duration in {< 1 year,1 - 4 years,4 - 7 years,

## : : : unemployed}: no (17.3/1.6)

## : : employment_duration = > 7 years: yes (8/1.2)

## : job = unskilled:

## : :...months_loan_duration <= 26: no (59/19.7)

## : : months_loan_duration > 26: yes (3.3)

## : job = skilled:

## : :...purpose in {business,car0,education,

## : : renovations}: yes (16.6/4.1)

## : purpose = car:

## : :...dependents <= 1: yes (27.7/10.6)

## : : dependents > 1: no (8.1/1.4)

## : purpose = furniture/appliances:

## : :...years_at_residence <= 1: no (18.7/6.5)

## : years_at_residence > 1:

## : :...other_credit = bank: yes (4.5)

## : other_credit = store: no (2.3)

## : other_credit = none:

## : :...percent_of_income <= 3: yes (33.5/15)

## : percent_of_income > 3: no (27.3/9.3)

## checking_balance in {> 200 DM,unknown}:

## :...years_at_residence > 2: no (135.6/32.2)

## years_at_residence <= 2:

## :...months_loan_duration <= 8: no (12.9)

## months_loan_duration > 8:

## :...months_loan_duration <= 9: yes (10.4/1.3)

## months_loan_duration > 9:

## :...months_loan_duration <= 16: no (31.3/4.2)

## months_loan_duration > 16:

## :...purpose in {business,car0,renovations}: no (21.3/8.4)

## purpose = education: yes (6.3/0.8)

## purpose = car:

## :...credit_history in {critical,very good}: yes (17.3/2.6)

## : credit_history in {good,perfect,poor}: no (9.6)

## purpose = furniture/appliances:

## :...credit_history in {critical,perfect,

## : very good}: no (5.6)

## credit_history = poor: yes (4.9)

## credit_history = good:

## :...housing in {other,rent}: no (2.6)

## housing = own:

## :...age <= 25: no (6.8)

## age > 25: yes (29.2/10.2)

##

## ----- Trial 9: -----

##

## Decision tree:

##

## checking_balance = unknown:

## :...dependents > 1: no (26)

## : dependents <= 1:

## : :...amount <= 1474: no (39.7)

## : amount > 1474:

## : :...employment_duration in {> 7 years,4 - 7 years}:

## : :...years_at_residence > 2: no (21.8)

## : : years_at_residence <= 2:

## : : :...age <= 23: yes (4.1)

## : : age > 23: no (19.7/4.2)

## : employment_duration in {< 1 year,1 - 4 years,unemployed}:

## : :...purpose in {business,renovations}: yes (23.2/3.6)

## : purpose in {car,car0,education,furniture/appliances}:

## : :...other_credit in {bank,store}: yes (29.1/10.5)

## : other_credit = none:

## : :...purpose in {car,car0}: no (12.3)

## : purpose in {education,furniture/appliances}:

## : :...amount <= 4455: no (23.7/4.4)

## : amount > 4455: yes (11.1/1.3)

## checking_balance in {< 0 DM,> 200 DM,1 - 200 DM}:

## :...percent_of_income <= 2:

## :...amount > 11054: yes (15.7/3.6)

## : amount <= 11054:

## : :...savings_balance in {> 1000 DM,500 - 1000 DM,

## : : unknown}: no (41.5/11.2)

## : savings_balance = 100 - 500 DM:

## : :...other_credit = bank: no (5.1)

## : : other_credit in {none,store}: yes (21.7/9.4)

## : savings_balance = < 100 DM:

## : :...employment_duration in {> 7 years,unemployed}: no (34.6/11.5)

## : employment_duration = 1 - 4 years:

## : :...job = management: yes (5.1/0.8)

## : : job in {skilled,unemployed,unskilled}: no (65.4/15.8)

## : employment_duration = < 1 year:

## : :...amount <= 2327:

## : : :...age <= 34: yes (20.5/1.9)

## : : : age > 34: no (3)

## : : amount > 2327:

## : : :...other_credit = bank: yes (2.8)

## : : other_credit in {none,store}: no (20.1/3.9)

## : employment_duration = 4 - 7 years:

## : :...dependents > 1: no (4.6)

## : dependents <= 1:

## : :...amount <= 6527: no (16.8/7.2)

## : amount > 6527: yes (7)

## percent_of_income > 2:

## :...housing = rent:

## :...checking_balance in {< 0 DM,1 - 200 DM}: yes (69/22.1)

## : checking_balance = > 200 DM: no (3.4)

## housing = other:

## :...existing_loans_count > 1: yes (18.7/5.3)

## : existing_loans_count <= 1:

## : :...savings_balance in {< 100 DM,> 1000 DM,

## : : 500 - 1000 DM}: yes (29.1/8.6)

## : savings_balance in {100 - 500 DM,unknown}: no (15.3/3.2)

## housing = own:

## :...credit_history in {perfect,poor}: yes (26.9/7.4)

## credit_history = very good: no (14.9/5.6)

## credit_history = critical:

## :...other_credit = bank: yes (11.7/3.4)

## : other_credit in {none,store}: no (63/20.3)

## credit_history = good:

## :...other_credit = store: yes (8.9/1.4)

## other_credit in {bank,none}:

## :...age > 54: no (9.5)

## age <= 54:

## :...existing_loans_count > 1: no (10.2/2.7)

## existing_loans_count <= 1:

## :...purpose in {business,renovations}: no (10.1/3.6)

## purpose in {car0,education}: yes (4.7)

## purpose = car:

## :...other_credit = bank: yes (4.9)

## : other_credit = none:

## : :...years_at_residence > 2: no (14.8/4.5)

## : years_at_residence <= 2:

## : :...amount <= 2150: no (14.9/6.2)

## : amount > 2150: yes (11.1)

## purpose = furniture/appliances:

## :...savings_balance = 100 - 500 DM: yes (3.8)

## savings_balance in {> 1000 DM,

## : 500 - 1000 DM}: no (2.8)

## savings_balance in {< 100 DM,unknown}:

## :...months_loan_duration > 39: yes (3.3)

## months_loan_duration <= 39:

## :...dependents <= 1: no (57.6/19.4)

## dependents > 1: yes (4.6/1.1)

##

##

## Evaluation on training data (900 cases):

##

## Trial Decision Tree

## ----- ----------------

## Size Errors

##

## 0 56 133(14.8%)

## 1 34 211(23.4%)

## 2 39 201(22.3%)

## 3 47 179(19.9%)

## 4 46 174(19.3%)

## 5 50 197(21.9%)

## 6 55 187(20.8%)

## 7 50 190(21.1%)

## 8 51 192(21.3%)

## 9 47 169(18.8%)

## boost 34( 3.8%) <<

##

##

## (a) (b) <-classified as

## ---- ----

## 629 4 (a): class no

## 30 237 (b): class yes

##

##

## Attribute usage:

##

## 100.00% checking_balance

## 100.00% purpose

## 97.11% years_at_residence

## 96.67% employment_duration

## 94.78% credit_history

## 94.67% other_credit

## 92.56% job

## 92.11% percent_of_income

## 90.33% amount

## 85.11% months_loan_duration

## 82.78% age

## 82.78% existing_loans_count

## 75.78% dependents

## 71.56% housing

## 70.78% savings_balance

## 49.22% phone

##

##

## Time: 0.1 secs

- The classifier made 34 mistakes on 900 training examples for an error rate of 3.8 percent. This is quite an improvement over the 13.9 percent training error rate we noted before adding boosting

credit_boost_pred10 <- predict(credit_boost10, credit_test)

CrossTable(credit_test$default, credit_boost_pred10, prop.chisq = FALSE, prop.c = FALSE, prop.r = FALSE, dnn = c('actual default', 'predicted default'))

##

##

## Cell Contents

## |-------------------------|

## | N |

## | N / Table Total |

## |-------------------------|

##

##

## Total Observations in Table: 100

##

##

## | predicted default

## actual default | no | yes | Row Total |

## ---------------|-----------|-----------|-----------|

## no | 62 | 5 | 67 |

## | 0.620 | 0.050 | |

## ---------------|-----------|-----------|-----------|

## yes | 13 | 20 | 33 |

## | 0.130 | 0.200 | |

## ---------------|-----------|-----------|-----------|

## Column Total | 75 | 25 | 100 |

## ---------------|-----------|-----------|-----------|

##

##

- We reduced the total error rate from 27 percent prior to boosting down to 18 percent in the boosted model.

- The model is still not doing well at predicting defaults, predicting only 20/33 = 61% correctly.

Making mistakes more costlier than others

Assign a penalty to different types of errors, in order to discourage a tree from making more costly mistakes. The penalties are designated in a cost matrix, which specifies how much costlier each error is, relative to any other prediction.

-

Specify the dimensions

matrix_dimensions <- list(c(“no”, “yes”), c(“no”, “yes”)) names(matrix_dimensions) <- c(“predicted”, “actual”) matrix_dimensions

## $predicted ## [1] “no” “yes” ## ## $actual ## [1] “no” “yes”

-

Assign the penalty for the various types of errors by supplying four values to fill the matrix.

error_cost <- matrix(c(0, 1, 4, 0), nrow = 2, dimnames = matrix_dimensions) error_cost

## actual ## predicted no yes ## no 0 4 ## yes 1 0

-

A false negative has a cost of 4 versus a false positive’s cost of 1.

credit_cost <- C5.0(credit_train[-17], credit_train$default, costs = error_cost) credit_cost_pred <- predict(credit_cost, credit_test) CrossTable(credit_test$default, credit_cost_pred, prop.chisq = FALSE, prop.c = FALSE, prop.r = FALSE, dnn = c(‘actual default’, ‘predicted default’))

## ##

## Cell Contents ## |————————-| ## | N | ## | N / Table Total | ## |————————-| ## ##

## Total Observations in Table: 100 ## ##

## | predicted default ## actual default | no | yes | Row Total | ## —————|———–|———–|———–| ## no | 37 | 30 | 67 | ## | 0.370 | 0.300 | | ## —————|———–|———–|———–| ## yes | 7 | 26 | 33 | ## | 0.070 | 0.260 | | ## —————|———–|———–|———–| ## Column Total | 44 | 56 | 100 | ## —————|———–|———–|———–| ## ## - This version makes more mistakes overall: 37 percent error here versus 18 percent in the boosted case. However, the types of mistakes are very different. Where the previous models incorrectly classified only 42 and 61 percent of defaults correctly, in this model, 79 percent of the actual defaults were predicted to be non-defaults.

- This trade resulting in a reduction of false negatives at the expense of increasing false positives may be acceptable if our cost estimates were accurate.